High and Low Notes from the ATA Conference

The timing for the annual American Telehealth Association (ATA) conference, which occurred last week, was far from ideal. The recent dip in the public market for telehealth companies led to a less than inspiring event which, according to most vendors, was significantly slower than ATA’21.

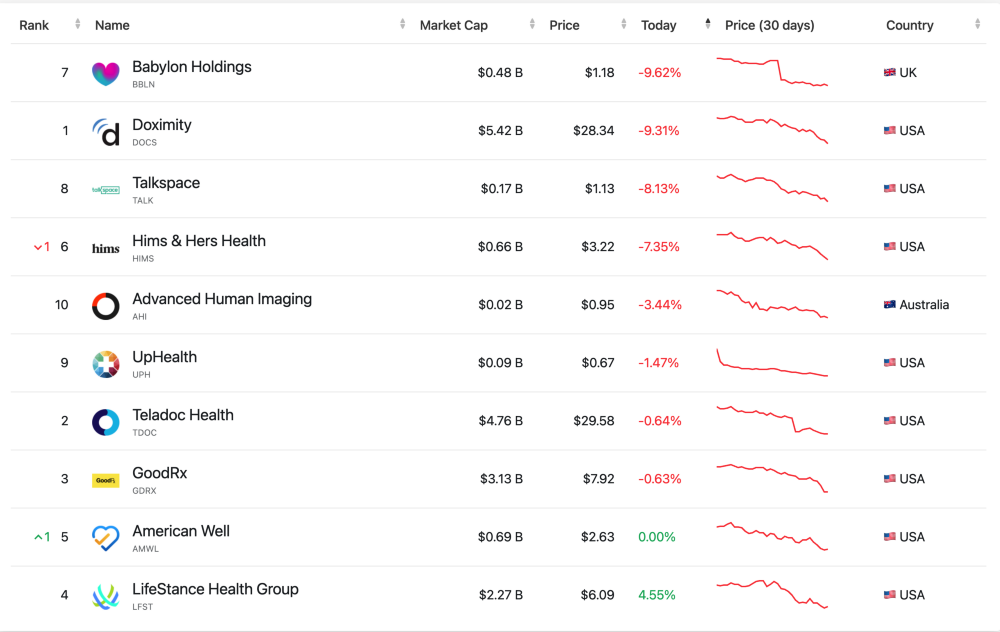

Teladoc shares plummeted roughly 42% the week prior on a weak forward-looking forecast and an over $6B write-off for the Livongo acquisition. Amwell’s stock is not faring any better, continuing its downward journey from its January 2021 peak. In fact, the whole telehealth market is going through major correction following the heyday of COVID, when in-person visits were put on hold.

Have we finally seen the bubble burst? With too high a supply in telehealth services and a precipitous drop in demand, a number of loud signals have been broadcasted before the storm crushed the telehealth coastline.

A big advantage of ATA’22 was an opportunity to speak with different vendors with no rush. Some booths had more traffic than others, such as Caregility, Current Health, and TytoCare, but the overall atmosphere was far from staid. Lots of booths were empty throughout the show, with many of the exhibitors’ efforts being wasted.

One major question: Where will big telehealth vendors go?

Virtual behavioral health visits have always been attractive to patients for a host of reasons. Thus, the big dip we have seen in telehealth visits for standard care has not been reflected in behavioral health visits. They will remain the biggest opportunity for sustainable growth in telehealth as a nation-wide shortage of mental health providers, especially in remote areas. Per American Addiction Centers data, behavioral health providers in the USA will reach an unprecedented shortage of 15,000 professionals by 2025.

A significant rise in behavioral health needs, much of it a result of a long-lasted pandemia especially in the younger population. Most big telehealth vendors have behavioral health offerings now. However, most of these telehealth vendors have only recently offered virtual, behavioral health services. In their Q1’22 investor call, Talkspace, who focuses on telehealth services for behavioral health, was one of the few telehealth vendors reporting good results.

ATA’22 was a good place to rethink post-pandemic health economy trends. The CEO of Biointellisence, James Mault, has no doubt that asynchronous health will get a good share of the pie with the regression of the telehealth market. With a good level of confidence, digital solutions allowing more providers’ time spending and preserving/increasing patient satisfaction will be on the rise.

There is also a lot of activity around Remote Patient Monitoring (RPM) with the recent funding success of Biofourmis and a number of larger companies getting into this market (Best Buy’s acquisition of Current Health), but to be clear, I have not seen any significant progress in complete PRM solution offering. Withings launched their RPM platform on May 2nd; they are definitely one of the companies to watch with a quite unique patient approach. Antoine Robillard, VP at Withings Health Solutions, shared his perspective on the RPM market growth, closely knit with increasing patient engagement.

With all these market corrections and a high supply of telehealth vendors, it will be interesting to see how the picture evolves over the next year. The tree of telehealth is definitely shaking, but maybe now we can start seeing the forest behind it.

With all of the highs and lows of ATA’22, it was great connecting with Chilmark Research clients and talking to vendors in-person. I hope all attendees enjoyed their time in Boston and returned home safely.

0 Comments