The Future of Clinician-Centric Innovation

Much has been written about this $28.3 billion monster acquisition. Most articles focused on what this means for Oracle and Cerner, yet little has been said as to what this may mean to the broader healthcare IT sector. In my musings below, I hope to clarify some of the longer-term repercussions of this acquisition.

Oracle knows how to make big enterprise software acquisitions – they’ll profit from snapping up Cerner.

Oracle is arguably the most successful company in making large enterprise acquisitions and capitalizing upon them; I wrote about this way back in 2008 when I pondered what would happen if Oracle acquired Cerner.

Oracle has made a number of such acquisitions in the past, including Peoplesoft. Core to their model is stripping a company down to bare essentials and raising maintenance revenue fees.

It remains to be seen how Oracle will treat Cerner going forward, as they have set up Cerner as a stand-alone division within Oracle that may provide some autonomy. Also, unlike previous acquisitions, where Oracle had some domain expertise, Oracle has exceedingly little in the provider market and will be heavily dependent on Cerner to make this acquisition work.

That being said, Oracle paid a lot for Cerner, and it will all come down to execution, especially taking Cerner into new markets overseas. Also, with such a large spend on Cerner, it remains to be seen what Oracle’s appetite will be to fund R&D within Cerner, which is sorely needed. My hunch is that Cerner will have to rely on its own internal resources to fund such advancements.

This is a win for Cerner investors; the jury is out on Cerner employees and clients.

Cerner investors have found a good exit with the Oracle purchase of Cerner, especially as it is an all-cash deal. They are happy. But to cover the costs of this acquisition, Oracle will likely continue Cerner’s selective closure of less profitable lines of business with subsequent layoffs.

Cerner clients, who have seen a drop in Cerner’s support and product enhancement capabilities—by and large a function of resources dedicated to the massive VA/DoD roll-out—will not see any drastic improvement in service and feature/function roll-outs for the foreseeable future.

However, there will be two glimmers of light. The first will reside in Cerner’s new RCM platform, RevElate, that will go GA later this year, the second, their life science data play, Cerner Enviza. Oracle has a wealth of experience in the FinTech arena that can be leveraged to further build upon RevElate, a long overdue viable RCM solution from Cerner. Oracle also has a very robust business in the life sciences market; Enviza will be an excellent tuck-in for Oracle.

The acquisition will not accelerate the move to cloud for Cerner; if anything, this will disrupt advances to date.

Much has been reported, including from Oracle, about how this acquisition will accelerate the growth of Oracle’s public cloud initiative, which is way behind AWS, MSFT and GOOG in the market. This is a feint to satisfy Oracle investors, many of whom were not that supportive of this acquisition, having preferred Oracle put that cash directly to work on the cloud.

Several issues will hinder taking Cerner to the cloud:

- First is the current deal Cerner has with AWS. There are likely both contractual obligations and client obligations to continue to support those solutions (HealtheIntent and CareAware) that currently sit on AWS.

- Secondly, though Cerner is built on top of Oracle’s database, it still will not be a walk in the park to migrate Cerner’s core product, Millennium, to the cloud. This will take years to complete.

- Third, in the future, large enterprises will take a multi-cloud approach that will be highly dependent on the use case at hand. Sure, certain applications may reside in a single cloud, but clients will want flexibility to leverage the strengths of other public clouds as well as hybrid.

- Lastly, the Kronos debacle also highlights the risk of the cloud, with many healthcare organizations hitting the pause button on their cloud migration efforts.

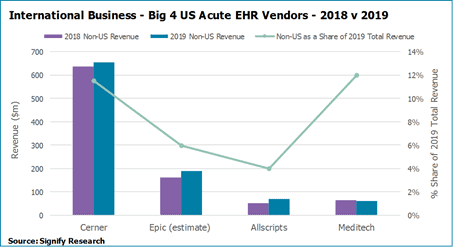

Epic stands on its own and will be the primary beneficiary in the U.S. market, but Oracle’s presence in international markets may tell a different story.

Epic has continued to gain market share on Cerner in recent years since the passing of Cerner founder and CEO, Neal Patterson. Neal was a visionary leader with a strong presence. However, that vision sometimes got in the way of the brass tacks needs of Cerner’s customer base – a strong ambulatory solution and equally robust RCM solution, two capabilities Epic did well.

Despite these losses, Cerner still holds a strong number two position in the U.S. and has been the most successful U.S.-based EHR vendor selling overseas. The ambulatory solution is improving and the aforementioned RevElate could stem the tide of losses, if not reverse them.

Epic will continue to gain significant market share at the expense of Cerner over the next 3-5 years, particularly among Cerner’s larger client accounts, as they weigh the risks of staying with the company versus defecting. But Cerner also has an opportunity to gain significant market share overseas by leveraging the Oracle sales force.

MEDITECH will also be a beneficiary of this acquisition at the lower end of market, especially the community hospital market, where Cerner had made some in-roads. Allscripts and CPSI will see little, if any, benefit from this acquisition.

What strikes me most is the need to completely rearchitect the EHR, from what was pushed upon the market as a result of the HITECH Act, to one that truly supports clinicians in the care of their patients.

Accelerate acquisitions and consolidation of remaining EHR vendors.

Yes, Oracle paid a lot for Cerner, but it was worth it? Cerner is the only target in the entire provider health IT space with such gravitas and market/mind share that was available for purchase. Epic, per CEO/founder Faulkner’s edict, will never go public and is unlikely to be sold. MEDITECH is still firmly in the control of one of its founders and not for sale.

But the acquisition will trigger a number of future acquisitions in near future. In the acute care EHR market, Allscripts, as a public company, will likely be acquired at some point. I would not be surprised if a PE firm picks them up and sells off the pieces. NextGen, another public company in the multispecialty, ambulatory market will be acquired. CPSI, who serves very small hospitals, while public, is hardly a stand-alone acquisition but will likely be folded into other EHR acquisitions as part of a roll-up strategy, such as what Harris has been doing as of late or even Point Click Care.

Innovation in the EHR market, which has been slowing, will decelerate further.

This last repercussion saddens me the most. Without a strong competitor such as Cerner, it will be difficult for competing EHR companies to continue to innovate and stay ahead as there is little motivation. Rather, those R&D resources will likely be applied to sustaining the base and build-out of bare minimum add-on solutions to sell into their base and keep those revenue numbers up.

Another avenue that will likely be explored is how to leverage existing provider relationships and clinical data for serving other markets – after all, the EHR market is fully mature in the US. Epic has done very well with this in serving the payer market, and Allscripts is looking at the life sciences market with Veradigm. But in both cases, it is not about improving the end product that clinicians use on a daily basis.

As a “system of record,” EHR companies will increasingly become a platform for others to build upon, leveraging those data resources to serve a multitude of end user needs via “systems of engagement.” The recently promulgated interoperability rules will be an accelerant to this transition.

Concluding Thought

As I review of what I’ve written, what strikes me most is the need to completely rearchitect the EHR, from what was pushed upon the market as a result of the HITECH Act, to one that truly supports clinicians in the care of their patients.

I harken back to a visit I had with my doctor just after the massive go-live of Epic at Partners Healthcare here in Boston. When I asked him what he thought of Epic, he turned to me and said:

“Well, it appears to be good for billing, but doesn’t do a thing for me in the care of my patients.”

It is high time we build an EHR to serve clinicians first, not administrators and the CFO. Who amongst the incumbents will take up that challenge? Only time will tell.

Yes, the need continues for Electronic systems to drive care and care experience.

It’s always been about coordinating simple reliable access to organized and relevant info about the patient, needs for care and delivery system capabilities and resources.

If EHR 2.0 ends up using legacy EMRs as a data pipe, so be it. Whatever it takes to move toward a CareSystem!

Nice article summarizing the market, John/Chilmark.

John, good to hear from you – it has been quite some time.

And yes, incumbent EHRs can be the spine, but that is but a small, albeit important part of an entire vertebrate entity. So many other things required to be truly functional and thriving – same goes for healthcare organizations.

Nice article, John. I share your sadness in noting that this acquisition limits motivations for broader EHR innovation — by Cerner and by competitors. We’ve been reading about EHR 2.0 for over a decade. As you accurately describe, the new platform would focus on clinician workflow.

Not so sure about EHR rollups — the economies of scale are illusive. In a typical rollup, economies of scale are achieved when customers are moved to the acquiring’s company offering. When an EHR vendor is acquired, the acquiring company cannot simply “move” customers to their platform. Many customers could choose to migrate to a competitor platform. At the least, the acquiring company will have to continue to operate the acquired company’s EHR for several years to facilitate a migration.

Hello Vince. Good to hear from you and thanks for your comment.

Regarding EHR roll-up strategy, I do not see it as all that dissimilar to what occurred in the ERP market about 15-20yrs ago (just goes to show you how behind the times health IT is). Anyway, a couple of companies were very successful at this, Infor and SSI (Infor eventually acquired/merged with SSI). Their strategies were similar.

1. Acquire small ERP company with decent/loyal client base.

2. Slash SG&A costs as well as development costs (many heads will roll) and put that ERP solution on maintenance doing bare minimum to keep up with regulatory requirements.

3. Raise maintenance fees for that legacy ERP and promise customers that you’ll never sunset a product.

4. Pick one ERP solution that will receive all future R&D resources and be the path forward once a company decides to migrate off the legacy solution.

5. Offer incentives, discounts etc to encourage future migration to that state-of-the-art ERP solution in #4

Why this hasn’t been done yet in the EHR sector is beyond me as it was a very successful strategy for Infor/SSI across the smaller, niche ERP solutions. Believe this strategy would be very successful across ambulatory sector. Not so much specialty, but PCP/general medicine.

That a physician would say that Epic does nothing for them in the care of their patients is a sad reflection on that physician’s arrogance and ignorance (and perhaps on their implementation and training) – the largest and most prestigious institutions in the world use Epic and many struggle to keep up and take advantage of all its features and capabilities – That being said, I also believe that we can do far better in automatically bringing in key information and helping over-burdened clinicians with decision support.

As you know Ken, I have a lot of respect for Epic and believe Judy has done a very good job of listening to her customers. That being said, all too often I’ve heard from physicians that the EHR is the bane of their existence. Not convinced this is a fault of Epic, but more reflective of what EHRs were originally intended to do: capture and code encounters for payment. They were never really architected to provide true longitudinal care, which is what a physician seeks.

I have been a DBA for two different “EHR” systems (we call it “EMR”, as in Electronic Medical Record) for more than 25 years. The system I am most familiar with is Cerner Millennium, and I have been working with the system since its earliest days after they decided to use an Oracle database. In my country we do not have the Hitech act and we have publicly funded healthcare.

One of my bugbears is the extent to which American software systems prioritise “Revenue Cycle” over clinical considerations. It should not be forgotten that, while the USA spends more on Healthcare (and by extension Healthcare computing) than any other country, it is ranked very low internationally in terms of actual Health outcomes, on a population basis.

In technology terms, I am suspicious of EPIC, which is a descendant of Cache, which is a descendant of MUMPS. I know the people who make decisions on software purchases like the sort of pretty graphs and images that only a PR person can serve up. I know that MUMPS made a list of top X worst software ever. But that was a long time ago. Maybe they have ironed out the problems.

As an old programmer I like hard iron and remain suspicious of “the cloud”, but I can see that, managerially, that is where things are moving and I cannot hold back the tide. I note you said “It still will not be a walk in the park to migrate Cerner’s core product, Millennium, to the cloud.”. Well actually, we have done it, as a proof-of-concept. I was involved in the project as someone who knew Cerner Millennium.

I don’t like Cerner being taken over by Oracle, even though I have worked with both for over two decades. As you say, Oracle have a history of squeezing their customers, even more so than Cerner. They have a good RDBMS, I suspect better than EPIC. Cerner Millennium core is a solid and reliable system, even though they have gone overboard in buying in extra systems that have to be bolted on by fencing wire and duct tape. My expectation is that Cerner will go downhill from here. I hope I am wrong.