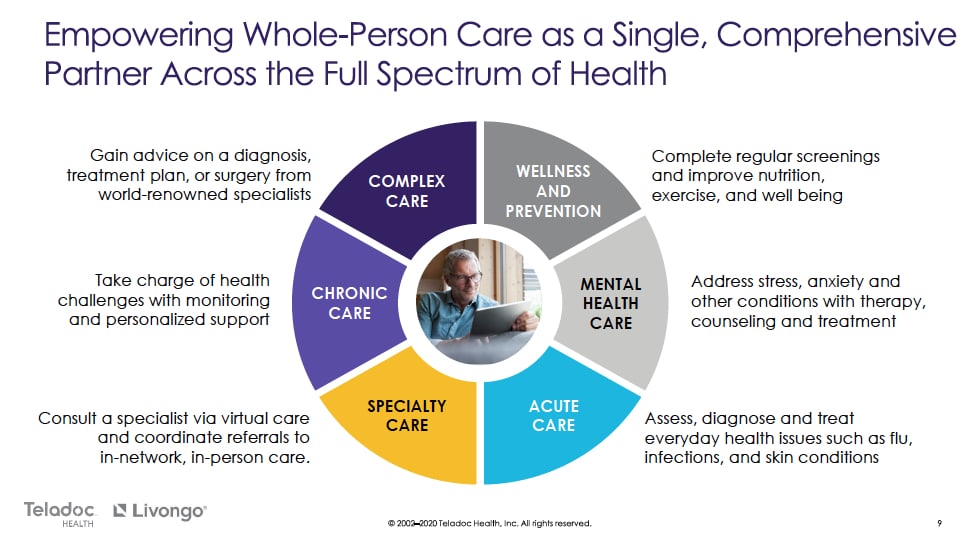

On August 5th, Teladoc (TDOC) announced that it would be acquiring fellow virtual care vendor...

Teladoc: The Virtual Care Platform the Market has been Waiting for

read more

On August 5th, Teladoc (TDOC) announced that it would be acquiring fellow virtual care vendor...

While these changes are being forced due to an episodic event, COVID-19, there is a strong likelihood that the changes will become systemic, forever changing how care is delivered.

We must have hit a batter’s slump in 2019. In past years, our predictions of what is to come have...

In this webinar, Senior Analyst Alex Lennox-Miller presents highlights from Chilmark's latest...

Last week, we attended the Connected Health Conference. While the intended audience was sometimes unclear, the buying priorities of providers and payers were clear: product integration and user-centered design for providers, with payers evaluating RPM, patient engagement and other population health management tools that they can offer as additional value to members.

Recently, Senior Analyst Alex Lennox-Miller was a guest on This Just In, a radio show and podcast...

![Quarterly Healthcare Meetup: New Front Doors to Care [VIDEO]](https://www.chilmarkresearch.com/wp-content/uploads/2019/04/front-door-to-care-networking-event.jpg?extend_cdn)

On March 27, 2019, Chilmark hosted the first in a series of Healthcare Meetups in Boston. Chilmark...

Our soon-to-be-released report, Primary Care for the 21st Century, reviews some of the changing...

This is the second in a series of blog posts recapping HIMSS'19; you can read all our coverage...