Healthcare continues trend toward consolidation as more M&A deals mark the end of 2017 As we...

Optum’s Deal With DaVita: Vertically Integrated Healthcare Continues to Grow

read more

Healthcare continues trend toward consolidation as more M&A deals mark the end of 2017 As we...

Yesterday, Chilmark Research participated in a webinar hosted by the eHealth Initiative. The topic...

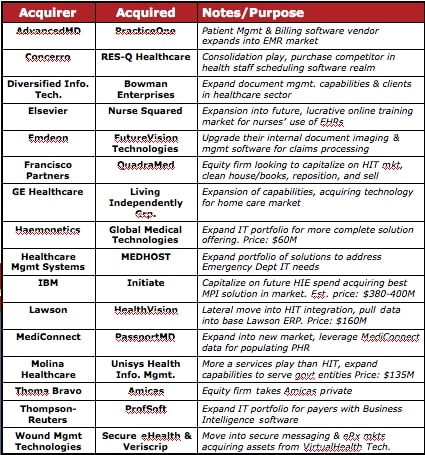

Since the beginning of 2010 there has been a series of acquisitions in healthcare IT (HIT) market,...

Doing some quick analysis of the healthcare IT market and have uncovered some 17 HIT software...