If you’d asked almost anyone in the healthcare IT industry about telehealth in mid-2020, their response would have been full of enthusiasm about finally unleashing all the promise telehealth had been teasing us with for years. With appointment volumes nearing 50% in some cases, the universal refrain was that now that patients and providers had experienced everything telehealth had to offer, there was no going back. As we approach the end of 2021, that casual confidence is risking us all the advances in acceptance and deployment that were made over the last eighteen months.

Key Takeaways

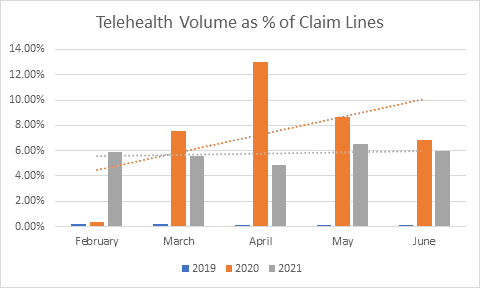

- Far from its peak in April and May of 2020, telehealth volume has roughly plateaued in the summer of 2021. More importantly, appointment types and volumes have shifted precipitously. Telehealth is moving back towards a niche teletherapy and urgent care solution.

- There are still significant barriers in ease of use, accessibility, and trust that virtual care vendors can no longer ignore if they want to increase long-term use and adoption of these solutions.

According to the Center for Connected Medicine, more than 80% of organizations are now doing less than 20% of their total patient visits via telehealth modalities. The types of appointments being offered have also shifted. In May of 2020, established patient visits, which lasted 15 and 30 minutes each and medical discussions were three of the top five billed CPT codes. In July of 2021, teletherapy codes had taken three of the top five spaces. While patients report wanting to use telehealth for non-urgent care, chronic condition management, and specialists, organizations are reducing the types of appointments they offer.

4 Reasons Telehealth and Virtual Care are Struggling

1. Concerns over profitability

As organizations look forward to the potential expiration of the reimbursement waivers that supported telehealth in 2020, they’re concerned that telehealth volume won’t meet their revenue needs. CMS proposals to extend telehealth billing codes are a good start, but permanent codes are needed. In addition, as the American Telemedicine Association stated in their comments to the 2022 Physician Fee Schedule, additional expansions of remote monitoring codes are needed to expand the number of providers who can offer these services, and to enable broader staff involvement in billable services.

2. Patients still prefer speaking directly with their provider

In September, ONC released a brief on the use of patient portals and smartphone apps in a survey that was conducted from January to April of 2020. Even with the limitations of its study period, the ONC data shows some important issues in the virtual care space. Pre-pandemic, about 70% of patients didn’t use their online portal or app for communication, preferring to speak with a provider directly. This number may have increased during the pandemic. It’s more likely, however, that patients are still deferring outreach and questions for remote appointments, not using messaging and triage apps.

3. Patients struggle with usability and design

The ONC reports that of the 70 percent of patients who did not use a patient portal, almost half of those were uncomfortable using a computer or found it too challenging to log-in and use patient portal apps. A focus on simple, patient-centric UIs that promote ease of access and use is needed for virtual care to be used consistently to have a meaningful impact. Increasing focus on consumer-style engagement may help alleviate these concerns, but as our upcoming Consumer and Patient Engagement report discusses, these are not the best methods to drive long-term engagement and clinical effectiveness.

4. Earning and retaining trust is tough

Trust remains the single largest barrier to adoption. According to ONC, 24% of non-users were concerned about the security and privacy of portals and apps, a population that has grown more than 70% since 2018. When it comes to patient confidence and long-term use, the greatest factor is provider recommendation and encouragement. Provider recommendations produce more engagement and longer usage of health apps even when the level of provider touch is very light.[1]

Unfortunately, provider trust is still difficult to earn and retain. Providers struggle to know which apps are the most effective, vetted, and safe to use. They often aren’t aware of validating and trustable sources[2], or local equivalents to the Australian Handbook of Non-Drug Interventions simply don’t exist. Majorities of providers would like to see authoritative data privacy standards and standardized quality criteria they could review, even outside of a mandated regulatory regime.

Organizational support in curating and supporting apps can help with these issues, but providers still report struggling to provide expert advice, feel undertrained, and worry about their professional liability.[3] Concern about increased use of AI/ML, the accuracy of algorithms and bias issues within them contributes even more. An increased focus on transparency and directly addressing provider trust issues needs to be a focus of every vendor in the virtual care space.

What comes next?

Telehealth won’t go away, but it can’t play the transformative role so many health systems want it to. Major telehealth stocks like Amwell and Teladoc have plummeted from their highs of 2020 and early 2021 and both are pivoting away from their dependence on synchronous telehealth, offering more asynchronous and home-based services. Employers and payers that represent the fastest growing buyer segment are focusing on remote monitoring and population health spaces. Health systems, however, are focusing on bringing patients back in-person. If those organizations want to retain their patients and have input into the development of these technologies and markets, they need to start taking home monitoring and chronic care technologies seriously and working to build up the policies and systems that are needed to support them.

[1] Pratap, A., Neto, E. C., Snyder, P., Stepnowsky, C., Elhadad, N., Grant, D., Mohebbi, M. H., Mooney, S., Suver, C., Wilbanks, J., Mangravite, L., Heagerty, P. J., Areán, P., & Omberg, L. (2020). Indicators of retention in remote digital health studies: a cross-study evaluation of 100,000 participants. NPJ Digital Medicine, 3, 21.

[2] Byambasuren, O., Beller, E., Hoffmann, T., & Glasziou, P. (2020). Barriers to and Facilitators of the Prescription of mHealth Apps in Australian General Practice: Qualitative Study. JMIR mHealth and uHealth, 8(7), e17447. https://doi.org/10.2196/17447

[3] Wangler, J., Jansky, M. The use of health apps in primary care—results from a survey amongst general practitioners in Germany. Wien Med Wochenschr 171, 148–156 (2021). https://doi.org/10.1007/s10354-021-00814-0

Very useful research about telehealth & virtual care. Thanks for sharing such an informatic topic with us.